By Paul Wright, SignValue.com

By Paul Wright, SignValue.com

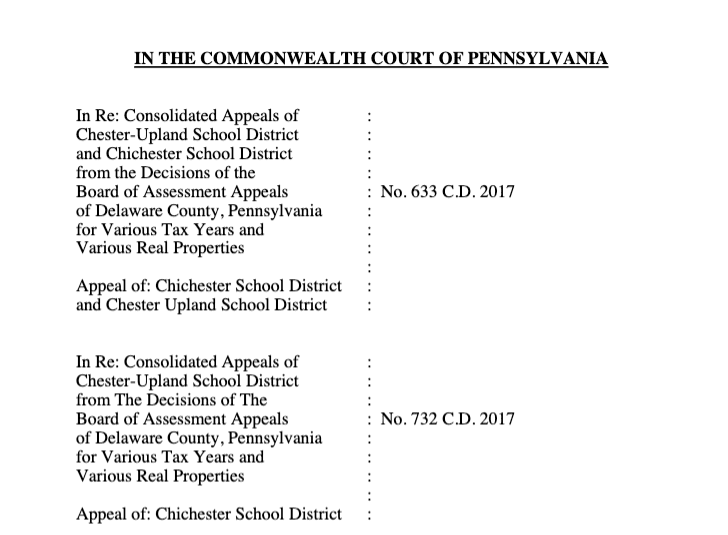

A very important tax case was recently decided in the Pennsylvania Commonwealth Court. Billboard owners and landowners should take note of the case and its potential long-term implications. The court concluded that billboard lease income can be considered when estimating the taxable value of land. In Pennsylvania billboard structures are taxed as personal property, so they cannot be included in the value of the property. However, the court recently ruled that the income that landowners receive is an important consideration in the tax assessment of the land.

This could be a seminal case for billboard lease tax assessment policies in Pennsylvania and nationwide. While most assessors in the United States tax billboards as personal property based on self-reported values, some may start to look at billboard lease income more closely. In addition, self-reported values of the cost to build billboard structures may also be scrutinized more heavily. Assessors that don’t have an inventory of billboards in their jurisdiction may start creating inventory lists to ensure that structure and lease values are fair and equitable.

You can read the entire court decision here.

[wpforms id=”9787″]

Paid Advertisement

What if the sign company owns the land the billboard is located on and no lease is paid?

Also, on normal billboard lease sites, is the tax based on the “actual” lease payment received or an “average” the tax assessor chooses?