By Craig Berry, Stark Capital Solutions

Stark Capital focuses in two niche Industries: Billboards and Cell Towers. Our two cents on the comment: “Towers are selling for 20-30 times tower cash flow, and typically getting over 20 offers per engagement” is a very accurate assessment of the current Tower M&A market.

Tower multiples are directly related to the number of tenants located on a tower at the time of a sale. Here is what our latest data suggests:

1 Tenant Towers- Avg. Deal Multiple: 34.7x

2 Tenant Towers- Avg. Deal Multiple: 27.9x

3 Tenant Towers- Avg. Deal Multiple: 20.3x

So, to the question of why aren’t billboards and towers selling for similar multiples?

As Billboard Insider previously pointed out- there are a number of fundamental characteristics in the Tower business model that differentiates from the traditional OOH plant, such as:

*Long-Term (25-year) leases with credit tenants.

*Built in annual escalators (3-5%).

*NNN Leases in some cases.

*Stable future cash flows.

*No creative, sales staff, vinyl changes, etc.

All of these passive and predictable characteristics lower the risk to a potential acquirer compared to billboard cash flow, which inherently comes with more risk. Classic investment theory is the lower the risk = the lower the return (as commonly seen in traditional real estate). Therefore, due to the lower risk, investors are willing to accept lower returns… which translates to higher multiples.

Secondly, the large consolidators in the Tower Industry can rationalize paying high multiples when they’re confident additional tenants will be added to the tower over time – this is why single tenant towers are traded at the highest multiples.

With Tower assets, once a second or third tenant are added, the cash flow will commonly triple or quadruple. This significant increase in cash flow ultimately drives down the buyer’s effective multiple paid.

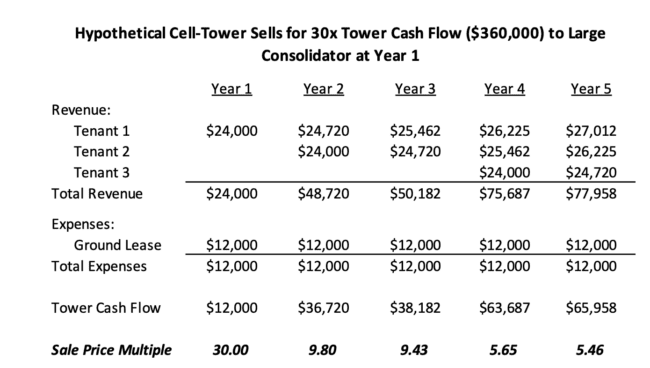

Take an example with the following assumptions:

*Tenant Agreements: $2,000/mo. with 3% annual escalators

*Ground Lease: Fixed $1,000/mo.

*Year 2: Second Tenant comes along

*Year 4: Third Tenant comes along

Generally speaking, when billboard companies are analyzing acquisitions, they’re betting on increasing sales or operating the assets more cost efficiently than the seller. This often results in slower and more modest cash flow growth over time, as opposed to the dramatic cash flow increases seen in the Tower Industry.

Lastly, Tower consolidators are bullish of the Industry due to the capital invested by Verizon, AT&T, and T-Mobile to build out the existing cellular infrastructure, which is all driven off the need for Towers. Unlike the Billboard Industry where the client has multiple advertising options at any given time, Tower companies hold a monopoly-like position on their clients for the foreseeable future.

One Final Thought: The grass isn’t always greener on the other side. In the Tower world, operators only have 3 potential tenants (4 if you count DISH) vs. Billboards who have virtually unlimited tenants. Once you factor in Tower construction cost of ~3x billboard cost, developers are putting a lot of chips on the table betting that their inside connections with at least 1 of 3 tenants will pay off.

[wpforms id=”9787″]

Paid Advertisement

What does a typical average full size tower cost to construct with only labor and materials for tower only?

It varies dramatically with the size of the tower. A 100-200 foot tower may cost a couple hundred thousand. A 1,000 foot tower is more than a million.