Insider thinks a public out of home REIT (e.g. Lamar and Outfront) has a sustainable leverage (Debt/Cashflow) of 3.5-4.0. A private out of home company which is under no pressure to pay dividends has a sustainable Debt/Cashflow ratio of 6.0. Sustainable leverage consists of how much money you can borrow and maintain your plant, pay your dividends and service debt without growing cashflow. It’s not sustainable to incur debt at a level which requires growing cashflow to avoid a default.

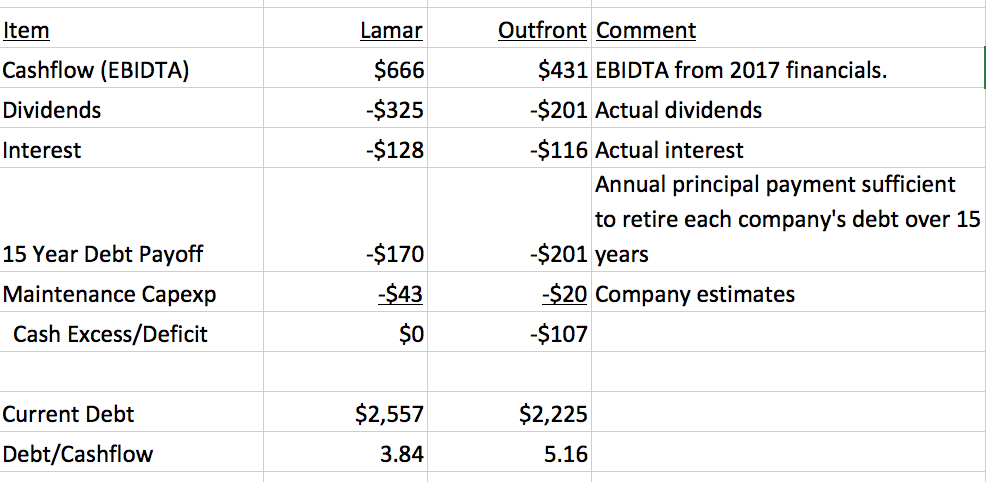

Look at this sustainable leverage analysis for Lamar and Outfront. If you assume that they want to meet current dividends and maintenance capital expenditures and pay off their debt over 15 years they shouldn’t borrow more than 4 times cashflow. At 3.8 times Debt/Cashflow Lamar has sustainable leverage because it can continue the dividend, maintain the plant and retire debt over 15 years without growing cashflow. At 5.16 times Debt/Cashflow, Outfront’s current leverage is not sustainable unless cashflow continues to grow.

Sustainable Leverage Analysis (000’s)

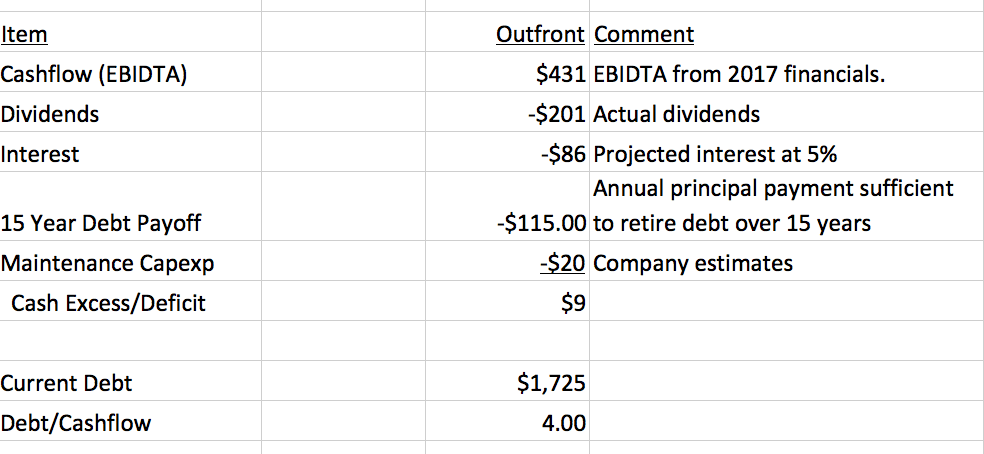

If Outfront reduced Debt/Cashflow to 4.0 then existing cashflow would be sufficient to meet the dividend and maintain the plant and retire debt.

Outfront’s Sustainable Leverage is 4.0 (000’s)

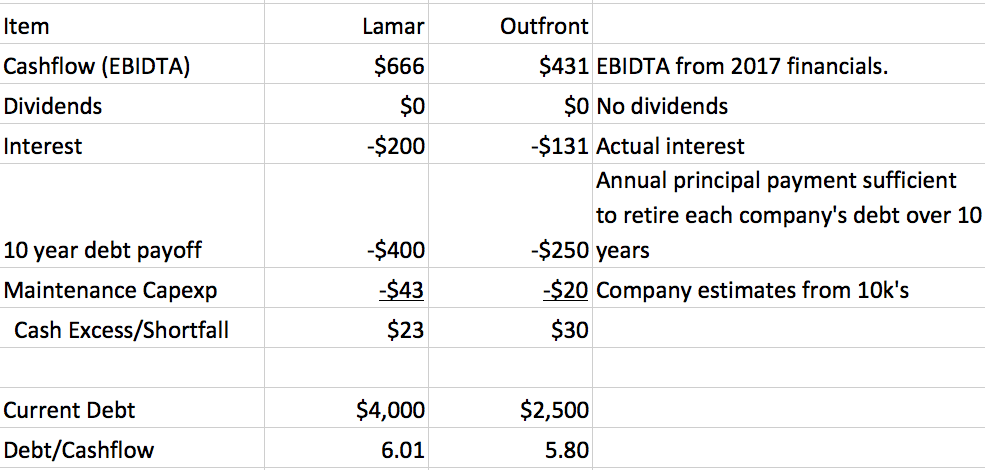

How does the analysis change for a private company? Let’s assume that Lamar and Outfront were private companies. There are no dividends but a private company’s lenders would probably want to see debt retired over 10 years as opposed to 15 years. That would equate to sustainable leverage (Debt/Cashflow) of 6.0:1.0.

No Dividends Mean Higher Sustainable Leverage (000’s)

There are four reasons for keeping your debt/cashflow below the maximum sustainable limit.

Rising interest rates. The fed has raised interest rates three times this year and Insider expects rates to continue to rise. An increase in interest rates will reduce sustainable leverage because interest expense will increase.

Capital Expenditures. Digital sign conversions and acquisitions take lots of money. If you are at 6 times Debt/Cashflow as a private company you will have little room to continue to make growth capital expenditures. You’ll be too busy paying back your lenders.

Operating Flexibility. When you borrow money your lenders will insist on financial covenants which restrict your ability to make acquisitions, pay dividends and make capital expenditures. High leverage means more restrictions on what you can and can’t do.

Digital Signs. Maintenance capital expenditure average 2-3% of revenues for a plant which consists of static steel monopole billboards with a 50 year life. Maintenance capital expenditures are much higher for a digital billboard because you’ll have to replace your LED’s at 100,000 hours or about 10.5 years. If your plant consists of digital signs you need to keep your leverage down in order to have room to handle higher maintenance capital expenditures. We’ll talk more about this in a future post.

What are your thoughts on sustainable leverage for an out of home company? Let Insider know using the form below.

[wpforms id=”8663″]

Paid Advertisement