Insider is always looking for articles that help us to better understand unique aspects of the OOH industry. Most of us are familiar with a REIT (Real Estate Investment Trusts) since Lamar and Outfront use that structure. However, understanding REITs and why they make sense for an outdoor company can be a little more confusing. The following article by Alex Pettee, CFA of Hoya Capital Real Estate provide some well informed background on tax implications for a REIT.

Insider did ask Alex why he thinks it make sense for OOH companies Lamar Advertising and Outfront Media to be in a REIT structure? His response follows:

“Specific to Billboard REITs, “REIT-status” awards these firms benefits beyond the tax code including additional analyst coverage, ample access to capital, and access to a vibrant community of REIT-focused investors that would otherwise overlook these companies.”

REITs and Taxes: An Overview

Since the creation of the Real Estate Investment Trust structure back in 1960, REITs have always seemed to be in the good graces of legislators and tax authorities. Under the goal of democratizing real estate investing for the masses, REITs enjoy significant tax advantages – most notably, avoiding double taxation – that are ultimately passed through to the end-investors. Investors often assume that these advantages must come with additional tax complications, which is generally not the case.

Put simply, REITs are far more tax-friendly and far less cumbersome for the end-investor than their complex-sounding name would otherwise imply. Functionally, from a tax reporting perspective, an investor’s experience with REITs shouldn’t be any different than a typical dividend-paying stock. Behind the scenes at the company level, however, it does get a bit more complex, as REIT distributions are composed of a mix of different tax characteristics, reflecting the underlying business activity of the REIT during the year.

We address four of the most common myths and misperceptions below.

Myth 1: REITs Are A Tax Headache

Fact: Taxes are always a headache, but REITs are no more of a headache than a typical dividend-paying stock, both of which report distributions at the end of each year on the standard Form 1099-DIV. Unlike MLPs or interests in partnerships or LLCs, REITs do not require K-1s or extra paperwork.

Myth 2: Don’t Hold REITs In Taxable Accounts

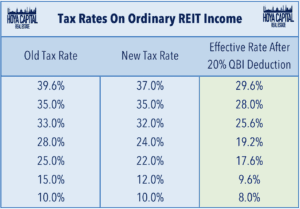

Fact: REIT investors were big winners from the 2017 Tax Cut and Jobs Act (TCJA), which essentially put REITs on par with typical qualified-dividend-paying companies when held in taxable accounts. Individuals are now permitted to deduct up to 20% of ordinary REIT dividends, which, in addition to the slight reduction in tax rates, amounts to an after-tax savings of 25%. The TCJA reduced the effective top marginal rate on Ordinary REIT Dividends – the bulk of the typical REIT distributions – from 39.5% to 29.6%.

Prior to the TCJA, we would generally advise our RIA clients to hold REITs in tax-advantaged accounts whenever possible. Assuming the average REIT distribution characteristics, investors across the income spectrum were paying significantly higher effective tax rates on REIT income than on qualified dividends under the old system. By significantly reducing the rates on Ordinary REIT Dividends while maintaining the rates on qualified dividends, however, the TJCA completely changed the equation.

Myth 3: REITs Are Exclusively Income-Oriented Vehicles

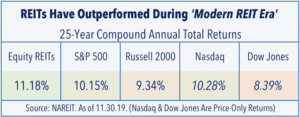

Fact: At the company level, REITs are able to retain significantly more capital than commonly believed, which has been a primary source of their under-appreciated historical record of strong growth. As we discussed in our Real Estate Decade in Review, while it may have been true decades ago that REITs were pure income-oriented vehicles, the Modern REIT Era has seen these companies evolve into dynamic, growth-oriented operating companies.

Myth 4: ETFs and Funds Don’t Enjoy the QBI Deduction

Fact: REIT investors got another win last year. The IRS amended an initially ambiguous regulation to allow ETFs and other REIT-owning Regulated Investment Companies (RICs) to pass-through the 20% QBI deduction to their shareholders. Investors owning REITs through ETFs, Mutual Funds, or Closed-End Funds are indeed eligible to receive the same favorable tax treatment of REIT distributions. This is especially critical as nearly half of REIT shares are owned through ETFs, mutual funds, and other types of RICs.

Summarizing Key Takeaways

Taxes are complicated and stressful, but REITs shouldn’t add any extra headache or paperwork to the dreaded year-end accounting. Functionally, from a tax reporting perspective, an investor’s experience with REITs shouldn’t be any different than a typical dividend-paying stock. REITs report using the standard 1099-DIV, not a K-1.

REIT investors were big winners from recent tax reform. Due to the new 20% QBI deduction, REITs are now essentially on par with typical qualified dividend-paying companies when held in taxable accounts. REIT investors got another win last year. The IRS amended an initially ambiguous regulation to allow ETFs and other REIT-owning funds to pass-through the QBI deduction to their shareholders.

Finally, while it may have been true decades ago that REITs were pure income-oriented vehicles, the Modern REIT Era has seen these companies evolve into dynamic, growth-oriented operating companies. At the company level, REITs are able to retain significantly more capital than commonly believed, which has been a primary source of their under-appreciated historical record of strong growth.

Insider Note: You can read the entire article at Seeking Alpha.

[wpforms id=”9787″]

Paid Advertisement