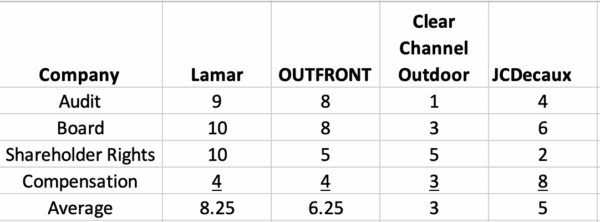

Here’s analysis of the governance of the public out of home advertising companies, sponsored and analyzed by SignValue. Institutional Shareholder Services (“ISS”) grades public companies on their governance and internal structures. It assigns a 1-10 ranking (1 good, 10 bad) to the following areas.

- Audit – Financial auditor independence, accounting controversies, extent of disclosures.

- Board – director independence, diversity and whether there are related party transactions.

- Shareholder Rights – Takeover defenses, voting procedures and whether there is one share one vote.

- Compensation – Pay for performance, non-executive pay, termination/severance agreements.

ISS scores evaluate the governance process, not outcomes. In fact, we have read a 2009 stanford study which concluded “governance ratings have either limited or no success in predicting firm performance or outcomes of interest to shareholders.” Here are the ISS scores for Lamar, OUTFRONT, Clear Channel Outdoor and JCDecaux as of June 2026 together with our comments.

Lamar

Why does the best-managed, best-financed, best-performing out of home company have the lowest corporate governance scores?

- Lamar’s audit score is low because it discloses less in financials than the other companies, because KPMG has been Lamar’s auditor for 10 years (ISS likes to see an audit tenure of less than 1o years) and because there are some insider transactions.

- Lamar’s board score is low because 3 of 10 board members are Reilly family (e.g. non-independent) and because average board tenure is in excess of 20 years. The ISS thinks that board members with more than 9 years tenure might not be as independent. Finally Lamar uses plurality voting for directors so a no vote for a director has no influence (see OUTFRONT discussion below)

- Lamar gets a low shareholder rights score because the the Reilly family owns Class B shares with supervoting privileges (10 votes per share versus only 1 vote per share for Lamar Class A shares) which give them control of the company.

- Lamar gets decent compensation scores. We think that Lamar execs are if anything underpaid.

Process is not performance. Lamar is a textbook case in why other things matter besides ISS scores. Yes the Reilly’s are in control but their net worth is highly concentrated in Lamar stock so they are rowing in the same direction as shareholders. Longevity – of employees, managers, execs and board members – is a key strength of Lamar. Nevertheless, we think Lamar can do a better job bringing in newer, younger board members.

OUTFRONT

- OUTFRONT’s low audit score of 8 probably reflects the fact that Price Cooper has been its auditor for 12 years and the ISS penalizes companies with auditor relationships above 10 years.

- OUTFRONT’s board score is a low 8 because OUTFRONT’s directors have an average tenure of 9.1 years which is at the high end of ISS standards.

- In the past year OUTFRONT improved it’s shareholder rights score from 10 in 2025 to a 5 in June 2026 instituting majority voting in place of plurality voting for directors. Majority voting means that you need to have more votes for than against in order to be elected as a director Plurality voting means that the director with the most votes wins, e.g. if you are the only director nominated and there is 1 vote for and 1 million votes against you are still elected. Majority voting is a win for shareholders.

- OUTFRONT’s compensation score declined from 2 in 2025 to 4 in June 2026. We suspect that this is because of large one time equity grants to Nick Brien upon his appointment as CEO. A score of 4 still is still better than average.

Financial performance is up and shareholders are getting more rights. A good story for OUTFRONT.

Clear Channel Outdoor

- Clear Channel Outdoor’s audit score has improved dramatically from an 8 in 2023 to a 1 in June 2026, reflecting the pending take-private acquisition. A company which is weeks from delisting has no long term auditor independence issues.

- Clear Channel has scored very poorly on compensation in the past as execs were paid well while the stock languished. Clear Channel improved dramatically to a 3 on compensation at June 2026 – the highest of the public out of home companies – due to the fact the stock has improved 71% in the past year. Execs were paid well but shareholders prospered.

JCDecaux

- JCDecaux gets a low 8 on compensation – the poorest in the public out of home group. Jean Francois Decaux was only paid about $3.4 million in 2025, versus compensation of $6-9 million for the US out of home CEOs. But the low score appears to be due to the fact that the JcDecaux exec team has few equity-linked forms of compensation as well as the fact that Decaux family members oversee the company’s boards which supervise, you guessed it, compensation for JCDecaux family members. The ISS is penalizing the company for a compensation conflict of interest, even though family members aren’t paying outrageous salaries to themselves.

If you have questions, contact one of SignValue’s experienced analysts for a free and confidential consultation at info@signvalue.com or call 480-657-8400.

To receive a free morning newsletter with each day’s Billboard insider articles email info@billboardinsider.com with the word “Subscribe” in the title. Our newsletter is free and we don’t sell our subscriber list.

Paid Advertisement