Insider wants to thank Brad Thomas of Seeking Alpha for allowing us to reprint his articles on the outdoor industry. Brad is a research analyst and he currently writes weekly for Forbes and Seeking Alpha where he maintains research on many publicly-listed REITs. In addition, he is the Editor of the Forbes Real Estate Investor, a monthly subscription-based newsletter. He is a shareholder and publisher on TheMaven (MVEN).

While we have spent time recently on Outfront and their MTA contract renewal, how the investment community perceives and values the larger Outdoor companies has impact on us all. The New York market represents 24% of Outfront’s total revenue and the MTA business is a large portion of that total. Seeking Alpha is a strong voice is the investment community and their opinions matter.

By Brad Thomas, Seeking Alpha

By Brad Thomas, Seeking Alpha

Summary

- I opted to wait for more clarity related to MTA, but now that is in the rear-view mirror, and there’s absolutely no reason to throw OUT “under the bus”.

- Now that the MTA deal is finalized, there is more clarity as it relates to OUT’s earnings stream – the forward runway (2018 AFFO/share forecast) is 13%.

- Show me another REIT that invests in New York City real estate that yields 5%?

My first research article on OUTFRONT Media (OUT) was on April 24th, and I concluded the article as follows:

“I see value in OUT, as a means to benefit from the continued growth in the US economy. Specifically, I am bullish as it relates to OUT’s superior assets (in top markets) and hard-to-replicate portfolio. OUT’s assets are located in prime, iconic locations and the cell tower leasing business should be an extremely profitable extension of the business.”

I did initiate a BUY rating and one reader commented as follows,

“OUT is waiting for a decision from the MTA. They are the incumbent, but there’s competition from Lamar and Intersection for this lucrative contract…If OUT doesn’t retain the business the stock will take a big hit.”

The reader was referring to New York OUT’s long-term deal with New York Metropolitan Transportation Authority (or MTA), the largest public transit authority in the country. The deal from the MTA gives OUT the ad and communications concessions for subway, commuter rail and buses along with billboards.

Last week, OUT announced that it had solidified the contract, and the billboard REIT will deploy more than 50,000 digital ad displays system-wide, installed on a rolling basis starting next year. It will also continue maintaining more than 500 billboard locations for the MTA.

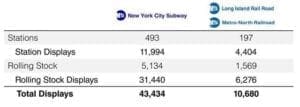

The MTA is North America’s largest transportation network, serving a population of 15.3 million people in New York City, Long Island, Southeastern New York State, and Connecticut. The MTA system includes 472 subway stations, 6,407 subway cars, 247 commuter rail stations, 2,429 commuter rail cars, and 1,255 buses.

“This contract represents an entirely new approach for the MTA, offering dramatically improved customer communications, and an upside potential for more advertising revenues,” commented Joseph Lhota, Chairman of the MTA.

“OUTFRONT Media’s commitment to installing digital screens in stations and on rolling stock will provide us with new ways of generating advertising revenue, while at the same time giving us a new platform to quickly and effectively get relevant information to our customers.”

In a more recent article (July 24th), I explained, “it may be time to initiate a position in OUT, I have now (as per my disclosure) forecasted Total Annual Return of 31% per year.” As my disclosure suggests, I own shares in OUT, but now that the MTA deal has been announced, I am increasing exposure. I opted to wait for more clarity, but now that is in the rear-view mirror, and there’s absolutely no reason to throw OUT “under the bus”. Shares are up ~6% since my last article…

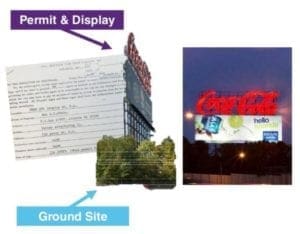

A Billboard REIT

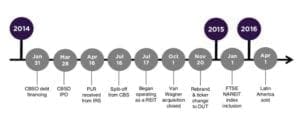

OUTFRONT Media is one of the largest out-of-home media companies in North America. The portfolio includes more than 400,000 digital and static displays, which are primarily located in the most iconic and high-traffic locations throughout the 25 largest markets in the U.S. The company went public on March 28, 2014, and began operating as a REIT on July 17, 2014.

OUT is also the advertising partner of choice for major municipal transit systems, reaching millions of commuters daily in the largest U.S. cities. OUT has displays in over 150 markets across the U.S. and Canada. According to a white paper:

“OUTFRONT connects brands to their target audiences, nationwide. Whether that audience be the techy, the business executive, the hipster, or the mom, OUTFRONT has it covered. Customized audience packages ensure brands reach the right consumer, at the right time, with the right messaging.”

Here’s a snapshot of the billboard asset components:

Bulletins (billboards) offer the most powerful impact of all outdoor advertising formats. Located on key highways, intersections, and integral choke points throughout the U.S., bulletins provide messaging with long-term presence and tremendous visibility to vehicular traffic.

OUT owns the permit for each billboard location and that provides the company with a competitive barrier to entry. OUT owns less than 10% of site locations; there are approximately 23,000 leases with 18,500 landlords (average eight-year life average). The majority of leases have abate and/or termination clauses for market weakness, and a small % have escalators.

In addition to billboards, OUT rents out wallscapes affixed to buildings in heavy traffic areas. These assets provide maximum impact for creative messages and are considered a great point-of-purchase exposure for creative districts. Wallscapes are perfect for penetrating urban centers and vary in size, providing endless creative options.

OUT’s transit franchise assets also provide complementary value to the billboard business in urban/suburban markets. Buses serve as “rolling billboards” traveling in and around densely populated city streets, leaving a lasting impact on pedestrians, motorists, and passengers. Eye-level bus exterior ads provide maximum exposure for customers.

Rail exterior also makes a huge impact, influenced by riders, onlookers, vehicular traffic alike, as they are waiting for the train to arrive or alongside major highways. Rail reaches a captive audience on their average 40-minute commute each way.

Digital brings numerous benefits to advertisers; it adds an extra layer of timeliness and relevance, and messaging can be easily changed.

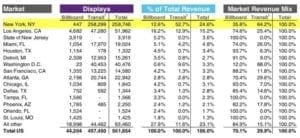

Here is a snapshot of OUT’s top markets (broken down by billboard and transit):

As you can see, New York is the largest market, representing around 24.6% of Total Revenue. Other top markets include Los Angeles (12.9%), Washington, DC (9.6%), and Miami (4.2%). OUT is also diversified by industry. Here is a snapshot of OUT’s Top 20 Advertisers based on “ad spending across all media”:

The Growth Strategy

As you can see below, OUT has four growth drivers:

OUT invests in key strategic locations (high traffic areas, transit centers, retail districts, and iconic locations). The company’s sales and operational incentives are aligned to maximize yield and profitability.

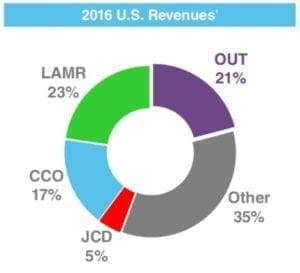

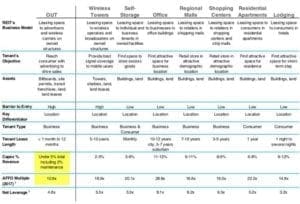

The US market is highly fragmented, as illustrated below:

One way to drive growth is by leasing out space on wireless carriers. OUT has 25,000 potential sites, and each site could hold 1-3 carriers. Wireless provides OUT with recurring monthly rent under long-term lease contracts with no capital expenditures required. The carriers are responsible for providing backhaul. The biggest catalyst for OUT is to create unique products and processes to drive media allocation.

OUT Mobile is an ad-tied platform that serves consumers within a geo-fenced area. This platform was launched in Q4-15 and drives strong secondary action rates.

Consumers’ travel patterns and behavior are represented in various formats (smartphones, billboards, mobile apps, ad cell carriers). OUT’s proprietary data management platform will associate the data to make it relational and contextual. Audiences will be mapped to OUT’s assets by day and time.

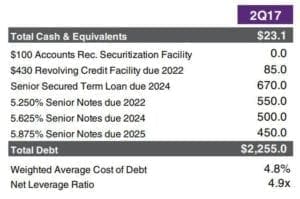

The Balance Sheet

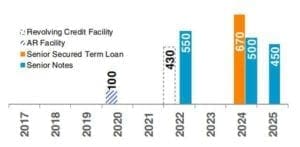

As of the end of Q2-17, OUT’s liquidity position was $466.6 million, including $23.1 million of cash, $343.5 million of availability on the revolving credit facility, and $100 million of availability under a new three-year accounts receivable securitization facility (entered on June 30).

The interest rate on that accounts receivable facility is favorable to the revolving credit facility by over 100 bps, and at the end of the quarter, OUT had $85 million drawn on the revolver ($50 million of that was used to pay the cash portion of the Canadian acquisition in mid-June).

In July OUT used the new accounts receivable facility to replace the drawn funds of the revolver. Due to the decline in OIBDA and a slight increase in net debt, OUT’s net leverage ratio has increased slightly to 4.9x. The company remains focused on its goal to reduce this to al longstanding target of 3.5x to 4x.vOUT and Lamar Advertising (NASDAQ:LAMR) are both rated BB- by S&P.

The Latest Earnings

In Q2-17, OUT reported revenues for the quarter were up 2.8%, and organic revenues were up 2.9%. Adjusted OIBDA was down just under 1%, a significant improvement from Q1-17. Despite the slight drop in OIBDA, AFFO was down 10% in the quarter due to higher maintenance CapEx and higher cash taxes.

In Q2-17, OUT grew revenues across both Billboard and Transit & Other in both the U.S. Media and Other. Transit & Other was the largest contributor to the reported 2.8% year-over-year growth this quarter. U.S. Media increased 3% on both a reported and organic basis.

Billboard organic revenues were up 0.2%, driven by strong local results, offset by a decline in national, which was an improved loss rate from the prior quarter. Both static and digital same board yields were down, slightly, at under 1%. Higher rates were offset by lower occupancy. Digital revenue was up high single digits and is over 15% of the company’s U.S. Media billboard revenue. U.S. Transit & Other was up 10.3%, organically, during the quarter.

OUT’s Canadian acquisition closed on June 14, and the company said it is “already seeing good traction in the third quarter as the new digital billboards, combined with (the) legacy static and digital displays, has doubled (the) daily audience impressions in the market and gives (the company) a leading platform for brands in the top markets in Canada”.

Also, in Q2-17, OUT’s reported expenses, excluding stock-based compensation, were up 4.5% year over year and up 0.4% for the six months. When you isolate the changes, the controllable U.S. expenses were flattish.

OUT’s capital expenditures were $25.6 million during the quarter, or 6.5% of total revenues. Growth spending was 4.6% of total revenues, and maintenance was 1.9%.

These are higher levels than seen historically, both in dollars and as a percentage of revenue. Maintenance primarily reflects safety vehicle spending that was needed. Growth reflects increased spending on digital initiatives, including the building and deployment of additional ON Smart transit displays as well as the building or conversion of 19 digital boards in the U.S. and seven in Canada, more than twice the level in total than in Q2-16.

For the quarter, AFFO was down 10.2%, primarily as a result of higher cash taxes and higher maintenance CapEx. The change in taxes reflects a benefit OUT had last year from CBS Corp. (NYSE:CBS) related to the split-off and the higher maintenance CapEx (noted above). For the six months ended June 30, AFFO was down 12% from last year. On a trailing 12-month basis, AFFO is essentially flat.

OUT’s 12-month trailing AFFO was $278 million, and dividend payout ratio was 70%, relative to the 67% in Q1-17. The increase is primarily due to higher maintenance CapEx and higher taxes. A payout ratio of around 70% is still right within the zone established when ONE went public and set its original dividend level.

OUT’s 12-month trailing free cash flow was $190 million, and the dividend payout ratio on this metric was 102%. On the earnings call, the CFO explained,

“The lower free cash flow number on a 12-month trailing basis is due to $10.1 million in higher CapEx and several abnormalities on our working capital this year. In particular, there was $29 million of working capital used on a trailing 12-month basis that when normalized would result in a much lower payout ratio of 89%.

First, there was a $9 million use that comes from the new Boston MBTA contract and a delay in receipts caused by systems issues within a large national advertising agency.

Secondly, and more importantly, our MTA contract extensions in 2017 have a very different payment structures than in the past. In 2016, we made six monthly payments with an annual revenue share true-up in the following year. In 2017, the extensions are structured to pay the actual revenue share amounts currently with no true-ups the following year.

As a result, in 2017, we not only paid the 2016 revenue share true-up but we’re also paying the higher revenue share currently. So this is not an indication of any increased cash use as much is it is a onetime change in timing.

These working capital matters have colored the cash flow generation calculation this year and are not an indication of the true cash flow of this business on a recurring basis. All of these working capital items will reverse themselves in 2018.”

Don’t Throw OUTFRONT Media Under the Bus

The wheels are on the bus (so to speak) as OUT now has the NYC MTA deal done. This $115 million deal (year one rent plus CPI bumps) is “accretive day one”, and cash flow should serve as a solid catalyst to support the company’s long-term growth objectives.

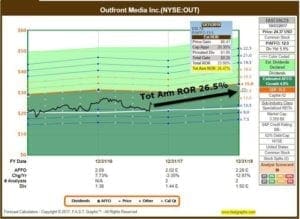

As evidenced by the snapshot below, OUT is still under-estimated when compared with other REITs:

Specifically, OUT is trading well below the peer P/AFFO multiple of other REITs.

Now that the MTA deal is finalized, there is more clarity as it relates to OUT’s earnings stream – the forward runway (2018 AFFO/share forecast) is 13% suggesting that a dividend increase of around 5% is likely.

Shares are up ~6% since my last article (in July 24), and I still find the dividend yield (or 5.9%) and P/AFFO multiple (of 12x) attractive.

There is certainly more risk since billboard revenue is dependent on ad spending. A weakening economy (or perhaps recession) could limit advertising and weaken the credit quality of some of the customers.

However, I’ll provide a more bullish reason for investing in OUT: Show me another REIT that invests in New York City real estate that yields 5%?

As I walk the streets of New York City (almost weekly), I am reminded that the real estate market is solid, and except for OUT, I have found no other REIT that provides me with a solid dividend and attractive (double digit) growth prospects.

To learn more about my REIT Beat service, click here. For a limited time, I am providing new subscribers with an autographed copy of The Intelligent REIT Investor. I plan to include my weekly BUY/SELL/HOLD list for all REIT Beat subscribers with all portfolios (weekly)

Note:Brad Thomas is a Wall Street writer, and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos, and be assured that he will do his best to correct any errors,if they are overlooked.

Finally, this article is free, and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking. If you have not followed him, please take five seconds and click his name above (top of the page).

Sources: FAST Graphs

Disclosure: I am/we are long APTS, ARI, BRX, BXMT, CCI, CHCT, CIO, CLDT, CONE, CORR, CUBE, DLR, DOC, EPR, EXR, FPI, GMRE, GPT, HASI, HTA, IRM, JCAP, KIM, LADR, LAND, LTC, MNR, NXRT, O, OHI, OUT, PEB, PEI, PK, QTS, ROIC, SKT, SPG, STAG, STOR, STWD, TCO, UBA, UNIT, VER, VTR, WPC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

[wpforms id=”9787″]

Paid Advertisement

![]()